The governing Council, the highest monetary policy body of the Central Bank, came together on Wednesday to a "non-monetary" session. As is clear from the confidential session, to the outside urge, should be the question discussed, such as the ECB buying now with the critical judgment of the Federal constitutional court to the bond program wants to bypass the PSPP. Great Controversies were not expected. As reported, there were signs in recent days that the Central Bank in a timely manner the documents could be put together, which could then be used by the Bundesbank prior to the summer recess of the Bundestag and the Federal government passed. Whether that is enough, the Federal constitutional court, would then remain to be seen.

Meanwhile, the chief economist of the ECB, Philip Lane, in an Online presentation explains why the ECB buys bonds, how it looks and what, without such purchases would happen – however, for the current crisis, not by the constitutional court challenged the old bond program of 2015. The starting point of his explanation is the Severity of the downturn in the economy. You should have indicators, which indicated a recovery in the economy, don't be fooled. "Loss of income and caution to be continued to save the consumer loads," said Lane. The recovery will continue: The gradual Opening up of the economy do in the short term significant growth progress possible. However, because of the extreme depth of the economic downturn in the pandemic, it will still take some time until the pre-crisis level will be reached again: "We do not believe that we will return before the end of 2022 to the level of 2019."

No Inflation in sight

Lane was also on the Inflation in the Euro area, which recently declined to almost zero. The net effect of the crisis on the Inflation will remain in the medium term to a considerable extent, "disinflation", will push Inflation downwards. The impact of the decline in the economic performance would offset any inflationary pressures through a crisis due to the restricted supply in the economy – like, for example, in the case of fruit and vegetables – more than.

On all of this now the ECB is reacting purchases with your bond. And from his point of view it was an "effective and efficient response", the ECB's chief economist. The ECB has managed to ease funding conditions for banks and also for companies and households. And you have to reduce the risk from the financial crisis, the financial crisis will melt with a "core of the financial markets".

Lane describes why in his view that the Central Bank is Central to not only influence the short-term risk-free interest rate ("Overnight Index Swap", OIS), but also the yields of government bonds. These were not, unlike often presented, only the cost of the States for their debts, but influenced as measuring the financing latte costs for banks, businesses and households in the Euro countries considerably. With the crisis, but the bond yields are ran by speculation apart again. The "Transmission", the Transmission of monetary policy to the bonds of the individual States, have only works for Federal loans well. Through the bond purchases in the crisis program PEPP, in which the proportion of each state can be handled bonds flexible, could mitigate this effect.

interest rate policy at present, less useful

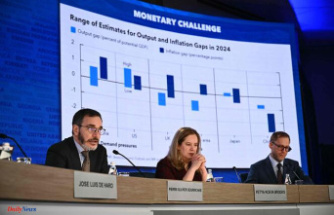

The ECB has to estimate how large the impact of the bond purchases are. The crisis program and the increase in the old program, APP, expressed as the premiums for government bonds with ten years to maturity, therefore, by almost 45 basis points. All the Central Bank interventions between March and June 2020 are expected to be the gross domestic product of the Eurozone for the years 2020, 2021 and 2022, accumulated to about 1.3 percentage points higher than without it. The Inflation, in turn, could fail during this period, in aggregate, approximately 0.8 percentage points higher than without the measures. "In these times, the benefits of the purchases are much larger than normal," said Lane, with a view to fundamental criticism of the bond purchases. Times of market Stress led to reductions to a lower effective interest rate. If the market conditions return to normal and the inflation Outlook would require then, is the ECB ready to cut interest rates further. At the Moment, but, says Lane, are bond purchases, the more efficient Instrument.

Date Of Update: 24 June 2020, 13:20