Recent economic history has shown how dangerous it is to lose your temper in times of crisis and panic as it is to leave things halfway and indulge complacently. The European economy and its institutions have responded to the pandemic and the war in Ukraine in a completely different way to what was seen in 2008, with initiative, forcefulness and speed, with "resilience and robustness". The worst was feared and it never happened, but now the shocks have reached the financial sector and crucial issues such as the conclusion of the Banking Union, the creation of a European Deposit Guarantee Fund, adding more entities to the community supervision and resolution umbrella and The ratification of the Mede, the mechanism that was created to rescue countries, is still up in the air. And just as disturbing are the market movements of these weeks as the apparent lack of blood among the continental leaders.

This Friday, Brussels has lived a Eurosummit. The Treaty on Stability, Coordination and Governance of the Economic and Monetary Union says that twice a year the heads of state and government must hold a Euro summit. They have not paid the slightest attention to the issue for a long time, which is resolved in a moment without much discussion and is settled with irrelevant conclusions. Today, once again, has been the case. The leaders have finished the week with a general discussion and a concise conclusions document, of just three points, and that does not even confront the elephants in the room.

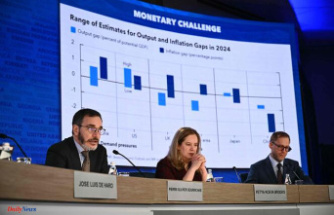

In the room were the 27, but also the president of the ECB, Christine Lagarde, and the president of the Eurogroup, Paschal Donohoe. According to Frankfurt sources, Lagarde told those present that the euro zone banking sector is resilient because it has strong capital and liquidity positions and internationally agreed regulatory reforms have been implemented, but that "recent developments remind us how important been to continually improve these standards" and that "we need to make progress in completing the Banking Union. Lagarde insists that there is no trade-off between price stability and financial stability", as the "toolbox allows us to address risks to both" and "to provide liquidity to the euro area financial system, if necessary ".

Nothing new, but also nothing sufficient by itself. The ECB has been complaining for 10 years that governments and fiscal policy have to do their part, that they cannot leave the responsibility in their hands. And if that was worth in good times, much more during turbulence and doubts.

Despite this, the agreed paper only has three vague points, such as that "the economic governance framework is a key pillar of the architecture of the Economic and Monetary Union, which supports the stability of the euro and the resilience of the economy of the euro zone", something as obvious as it is irrelevant. Or two references to the need for "intensified collective efforts, involving policy makers and market participants from across the Union, to move the Capital Markets Union forward" and "continued efforts to complete our Banking Union", as "it has considerably strengthened the resilience of the EU banking system".

It is striking, but despite the fact that the seams are visible with only a little turbulence, the 27 does not seem to be in any hurry. "Today's turbulence has not changed the position, there has not been any change in the conclusions previously raised," said the Spanish president, Pedro Sánchez, when asked if the leaders have addressed the situation this Friday in the room in the markets, when the shares of Deutsche Bank have fallen by 15 dragging the financial sector of the entire continent.

"We need to finalize the discussions on the Capital Markets Union, on the Banking Union. But not as a reaction to what happened in the US or to Credit Suisse. We think the current supervision is strong enough, but we still have to give the final steps", agreed the Dutchman Mark Rutte. It is no longer the US or Switzerland, or indirect blows, but the pressure is internal and the weakest link, the sharks seem to detect, is German.

The situation is tense, but the reaction is minimal. Everyone knows that it cannot be overstated, that any sign of panic would be interpreted in the worst possible light among investors and that as long as there is doubt the weakest links in relative terms, although not necessarily in absolute terms, will be the target. Hence the statements and the effort made to say that everything is fine. That part is normal, even logical. But what is not happening is that no steps are being taken to close the gaps. More than two dozen leaders took the floor in the economic debate, questioned Lagarde, warned of the risk of loss of confidence and conspired to avoid mistakes. But at the same time, the communiqué approved today expressly says that the work on the Banking Union must be done "in line with the Eurogroup declaration of June 16, 2022." What translated means, ignoring, once again, any work to complete the third pillar of the Banking Union: the European deposit guarantee fund.

The Banking Union has the first two pillars active, Supervision and Resolution, but a series of countries led by Germany have been preventing the third for a decade. They do not want to pool the deposit guarantee. On the other hand, Italy, due to a completely irrational and unbridled national reading, refuses to ratify the Mede Treaty, a mechanism that was reformed to give it more powers, once the era of bailouts was behind us. Donohoe demanded that Rome take the pending steps, but the issue is so toxic that Giorgia Meloni even decided to cancel the scheduled press conference to minimize the consequences of exposing herself to speaking.

The Eurogroup reference from last June is to throw in the towel, because that meant leaving aside the EDIS, the Deposit Guarantee Fund, in favor of a reinforcement of the national systems. Even the countries that have always claimed it, such as Spain, assume that it will not come out in the short or medium term. Germany, always worried about banks in the south, about defaults, exposure to sovereign debt, does not believe that this is the right time to pool more risks. But the one who was harassed by questions and had to go out this Friday to defend his entities and ask that the pending steps be taken was his chancellor, Olaf Scholz. When asked about Deutsche Bank, he assured that "its business model has been fundamentally modernized and reorganized and it is a very profitable bank. There is no cause for concern." How ironic.

According to the criteria of The Trust Project